Business

With the right representation, FIT Micro Finance Bank will lead the industry in terms of technology and various innovations – Okpe MD/CEO

Okpeh Andrew Ekoja is the Managing Director/CEO of FIT Micro Finance Bank Ltd. A banker who is driven to heights through determination and many years of experience. As the mantle rests on his shoulders to drive the new micro finance bank very soon, Okpeh in an exclusive interview with some journalist’s speaks on the strength of FIT MFB Ltd, their capital base, dealing with customers among other issues.

By Tony Edike

The FIT Group is coming up with a Micro Finance Bank come 5th December 2024, what formed this opinion?

Well, the unbanked and the Under-banked segment of the financial sector largely informed our decision to venture into the Micro finance industry. Although we intend to leverage on digital technology to create innovative solutions to ease banking challenges of these group that consist of over 65% of the banking population in Nigeria. We have partnered an IT Solution Firm, though organic but one of the best in the Micro Finance space to achieve our goals. We have also deployed a robust Core Banking Application CBA, top notch to meet our target profitably that is cost effective to maintain.

How ready are you as the pioneer MD of the bank to enter into the financial market, where today savings culture is going down due to hardship?

As the pioneer MD of FIT Micro Finance Bank Ltd, I am ready to take on the financial market by targeting the active Low- and medium-income class to grow them into wealth. We have carefully designed products & services that will encourage their saving culture despite the hard time with appreciable interest rate on the Daily Saving, group Saving, Micro Credits with friendly interest rate to help grow the business of MSME and also offer Free Financial Advisory session, helping them to navigate the difficult terrain of the present economy. We are also leveraging on some digital platforms to profile, track & recover credits advanced to our customers while partnering government MDAs grant loans to their workers and effectively monitor the repayments accordingly.

In Enugu, there are other Micro Finance institutions, how prepared are you to face the competitions and other conventional commercial banks?

Globally, the banking space is like an ocean. Irrespective of the age of these Banks in Enugu state with due respect to their owners, banking products are homogeneous differentiated by brands. Our strategy is speed, Accuracy, precision and customer satisfaction. This will be achieved through the experienced human capital in our team, Strategic managers and the robust Information Technology solution to make banking easy to our customers. Again, the products are Individual, Group and Corporate Savings accounts with good interest rate, Current accounts, Investment/Fixed deposits, Loans and Salary advance, Overdrafts. Cooperative account, Daily contributions, POS, ATM, FIT Mobile App, Salary Administration, Payment services & Housing loan for renovation.

As you are about to hit the ground running with the latest MFB, how much have you earmarked to support micro and small businesses in the first two years of its operations?

Our capital for the Micro Finance Bank is N200m. But we will surpass that, at the moment, we are at about N255m. That two now include the breakdown of people that have assets, both fixed asset and intangible asset. But by the regulation of Central Bank of Nigeria (CBN), it is not supposed to be in excess of 20% of that amount of money. So, what we set aside for business itself is in excess of N150m from micro credit to medium small businesses.

Though, we still have projections because we are looking to grow our deposit base further. So, for the next one year, we are looking forward to creating quality risk assess in excess of N200m. Our funds are going to come in from prospective investors who are the parent owners of this company. We are looking and target our high network customers within our axis who we have started meeting already and they are pledging to support us as we take off. In the next one year, we are looking forward to excess of N150m.

How prepared are you as the first MD/CEO to face competition given there are many established Micro Finance Banks (MFB’s) in the system already where today’s savings culture is going down due to hardship?

As the pioneer MD/CEO of FIT Micro Finance Bank Ltd, I am ready to take on the financial market by targeting the active Low- and medium-income class to grow them into wealth. We have carefully designed products & services that will encourage their saving culture despite the hard time with appreciable interest rate on the Daily Saving, group Saving, Micro Credits with friendly interest rate to help grow the business of MSME and also offer Free Financial Advisory session, helping them to navigate the difficult terrain of the present economy. We are also leveraging on some digital platforms to profile, track & recover credits advanced to our customers while partnering government MDAs grant loans to their workers and effectively monitor the repayments accordingly.

Again, I want to let you know that most MFB’s had long stayed in the system with mundane operations. But we are leveraging on digital innovations to reach out the unbanked and under-banked within the system which is a very wise thing that in Nigerian financial system they consist about 65-70% of the banking population.

So, how do you want to achieve this?

We have partnered with a global Information Technology (IT) company that in the past has over 20 years’ experience in Microfinance bank software. This allows us to function like what we have today in Monie Point, OPAY and PALMPAY etc. Our vision is to compete at that level because virtually in all the states in Nigeria, one does not see any branch of Monie point, but a whole lot of works is going on. Digitally, they are up there. Their systems are seamless and we are partnering our operations towards that too. Right now, at this stage we are leveraging on technology to reach out to these areas. For our internet service provider, we went a step further to launch through star link. It is a guarantee that with star link, the uptime is over 95%. Then in the next one year, my projection is that we too will leverage on the point of sales and it will not be less than N50,000 to reach out to all nooks and crannies of Enugu state, and the entire southeast and beyond. This is where the real money is. Every southeast operator that is using you on the site is an e-branch. From there they can open account do what we call payment services that transfers to further banks. They do cash transactions too and we support them. Now any that will approve custom there are those charges that will be shared between NINs, service provider and the bank itself. So, we are looking at the fact that for every transaction, our POS operators they do, out of that N100.00 or above will be earning about 45% of those money. It may look small, but cumulatively, depending on the total transactions per day, you will be arriving at a very substantial amount of money. Monie Point’s recent capital base is in excess of N1b Dollars. So, we want to leverage on that because we have the forms and the capacity to reach out the unbanked and under-banked sector in this system. With this, in one year, in the entire south east, FIT micro finance bank will be the number one in terms of technology, various innovations. With the artisans and market women all will be reached out to. We will be deploying and streaming our marketers with a device on their android. Out marketers can get to a shop owner with their device in your shop, you will get the account details with just minimal requirements to open that account.

How do you intend to go about this?

This android is empowered and digitally inclined to capture the customer’s deposit and post, then get the SMS alert of the credit of the money given to those agents in the field there and you get an alert immediately credited into your account. At that point, when they come back, we now reconcile the account and balance up their books. Now, we will provide security for them as they go on field. For the insurance, NDIC is there with them. For other insurance against theft, burglary, we are with Lead way Assurance already and our transactions are cloud free physical natural disasters might not affect us and we are putting up a strong Nigerian Data Protection Council (NDPC), our IT Head here is CISCO satisfied. He is on training with the NDPC to up his itinerary to see how our data’s while even the clouds are well protected with firewalls, so we cannot easily be hacked in. We have also deployed our websites where customers can get information about the bank, download forms and templates from there, subscribe to so many of our products and services where one can apply. One must not visit our location to assess our credit facilities. We are leveraging on technology, even help us further with special recognition, IT and address verification, utility bill will be very fine and so much more that we have done. Soon, I will consolidate my discussion with IPPIS authorities because when we give federal workers credit, and even the low income and middle-income earners can access our source, we will deduct ours as a partner of IPPIS. We are looking forward to doing so many innovations. The problem with the microfinance space which is a bonus is that every customer has as identity, for one to do any banking related transaction in Nigeria, one must have a Biometric Verification Number (BVN). BVN is one of the best collaterals in Nigeria.

With the ongoing tough economic reforms of President Tinubu administration, many are concerned that more Micro Finance Banks may soon collapse. Do you share this view and what in your opinion should government do to stabilize the industry?

I disagree with them because if one sets up a bank which is running smoothly, and are also guided by the policies and procedures of the regulatory authority, and working in agreement with what is correct; then the bank is a growing concern. Now you have money you have been trading over the time, if you follow the rules by the book and doing the right thing, there is a tendency for you not falling into the pit. The reason why some micro finance banks went under is because they are not mindful of what the regulatory authorities tell them. Most of them were one-man business that does as it pleases. The family members can come and take loans based on his approval and not based on credit approval. Even when they did not meet up with demands. Then when they do not pay, it becomes damage control. There are a lot of portfolios at risk in excess of the allowed able percentage which is not supposed to be more than 7% of one’s capital. Your bad loans are not supposed to be more than 7% of the capital to which one does business in the bank. But contrarily, one finds out that their percentage are in double digit which is a red flag already. Mosty of them already have liquidity issues in fixed deposit they are using to trade. FIT micro finance will not be like that. We tend to play by the books profitably. That is why we are deploying every necessary technology to our own advantage. The worst-case scenario is when it gets bad, one deploys legal means. Legal means could take another dimension like a legal court arbitration takes place, then both parties re-negotiate new terms to which that loan would be paid. At this point what one is supposed to do as a banker is to stop every interest on that loan because it has gone bad already. All penalties that will increase the amount, the customer has taken and what he has taken before as differential, then; it will be spread it to a thin line to which one will be able to meet with the obligations and finally clean the books.

Recently, cashless and technology failures in many banks have created fear in the mind of some customers that they industry is sick. Many now prefers to keep their money at home or with some fintech companies, what is your advice to such customers?

I am sure that before you put your money in a bank, google the bank. Find out about the bank. There are some banks in Nigeria that are very unhealthy. One should not take their money to those banks. Such customers are at their peril.

But banks would not let customers know this?

Yes, that is why I said we should not be carried away by emotional blackmail to deposit money in a bank that is about to go under. Now, before you put your money in bank, make your inquiries There are some banks in this country that has not submitted their audited financial statement in the last three years which is a red flag already. There are new banks who are coming up, very strong, check out their capital base, monitor them at the end of every financial year, find out the necessary things. Some of them have been removed from the stock market while gigantic buildings are still there. The world is a global community now, the Fintech drives the banking industry as we speak. Guess you do not know where Monie Point office is located.

I do not know where the offices of Monie point, Palm-pay and OPAY offices are located to make complaints.

The world is a global village now. My staff strength in FIT Micro Finance bank will not be more than 12 in number. All of them are computer literate. We work seamlessly, digitally and do everything humanly possible to keep the bank going. Then, our idea of innovation should be where to invest and when not to invest your money. Recently, the Federal government just released the sub-treasury bill for the month of November which is very sound, as a banker, one looks at it. Instead of leaving idle fund of about N150m in an account that will not generate anything, it will be advisable to buy a treasury bill of N90m, that is three months of about N60m; and at the end, one would be getting about N2,3 or 5m at the end of the day which will add up to the years profitability. Most MFB banks that are going under did not play by the rule. CBN rules is clearly stated that they should not give more than N2m to an individual or even a corporate account in MFB. If you want above that, then approach a commercial bank. But one will see some MFB giving between N8-10m loan to an individual. Customers are the sharks because they will be here when we launch, they will deploy all their money to impress us, but by the time they take the loan, we chase after them to recover. With my experience over the years, as customers are coming when we open, my loan to them will not be in excess of 18-months. The loan given to a customer will be monitored. Loan monitoring is key because most of these microfinance banks do not monitor their loans until it gets bad. If I take a loan from you and do not meet up with the first one month of my repayment, I should tell you that your account is in debit. If I did not see you within one week, I will find out what the problem is. We have also learnt the Stop-I falsification from the commercial bank called which means the business must be visited for evaluation of what you have and the amount you are requesting for

Fresh controversy has erupted over efforts to revive the sale of a 40 per cent stake in the Amukpe–Escravos Pipeline, with a governance expert warning that any attempt to resurrect a previously terminated transaction could damage investor confidence and raise fresh questions about transparency in Nigeria’s oil and gas sector.

Speaking on Channels Television on Thursday, June 11, 2026, Managing Director of Policy Management Consult Services, Jide Olatuyi, said concerns surrounding the transaction extend beyond commercial interests and strike at the heart of governance, transparency, and the credibility of Nigeria’s investment environment.

“The contract was terminated,” Olatuyi said. “What stakeholders are saying is that there is a need for a new competitive bidding process rather than attempting to revive a failed transaction.”

The controversy has intensified amid scrutiny of the asset’s valuation. The earlier transaction involving the 40 per cent stake was priced at approximately $243 million before collapsing over unmet contractual obligations. Independent assessments conducted in 2025 reportedly valued the same stake at between $544 million and $641 million.

The significant disparity between the earlier transaction price and the more recent valuations has fuelled calls for a fresh competitive bidding exercise to ensure that the asset reflects prevailing market conditions and delivers maximum value.

Rejecting suggestions that opposition to the proposed transaction is driven by sentiment or commercial rivalry, Olatuyi insisted that the debate centres on governance standards within the petroleum industry.

“I don’t think it is about sentiment at all,” he said. “It is about governance in the oil and gas sector.”

According to him, Nigeria’s challenge is no longer limited to attracting investors but also ensuring that investors have confidence in the integrity of the country’s commercial and regulatory processes.

“If you are not committed to transparency, it becomes a problem for investors,” he said. “If you cannot build trust and confidence in the sector, capital will go elsewhere.”

Olatuyi said several stakeholders, including project lenders such as Sterling Bank and AMCON, have advocated a transparent process that reflects current market realities and updated asset valuations.

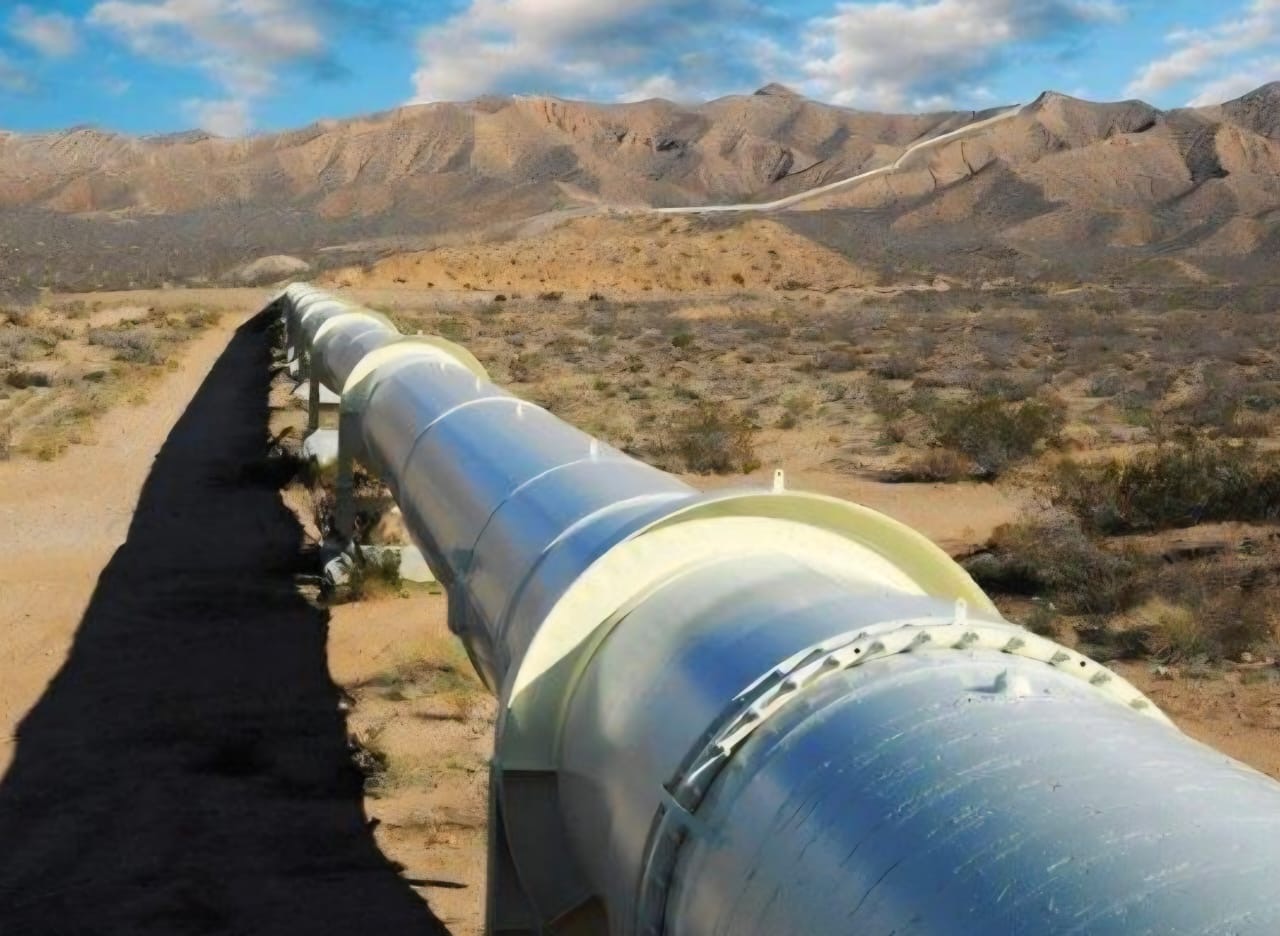

The Amukpe–Escravos Pipeline, which has a transportation capacity of about 160,000 barrels per day and has maintained uptime above 95 per cent, remains one of Nigeria’s most strategic crude evacuation assets. The pipeline plays a critical role in transporting crude from inland production fields to export terminals in the Niger Delta.

Olatuyi urged authorities to ensure that any future transaction involving the asset is conducted through an open, transparent, and competitive process capable of inspiring investor confidence and safeguarding public value.

The debate comes at a time when the Federal Government is seeking to attract substantial investment into the energy sector and expand critical oil and gas infrastructure.

The eventual outcome of the Amukpe–Escravos Pipeline transaction could serve as a major test of Nigeria’s commitment to transparency, valuation discipline, and investor protection. As global competition for energy capital intensifies, governance standards may prove just as important as resource endowment in determining where investment flows.

Officials of the Nigerian Upstream Petroleum Regulatory Commission and members of the technical committee that supervised the original transaction did not respond to requests for comment as of press time.

The Manufacturers Association of Nigeria (MAN) has raised alarm over the worsening state of manufacturing activities in the South-East, warning that rising energy costs and poor access to finance are forcing many companies in the region to shut down.

Chairman of MAN for Anambra, Enugu and Ebonyi states, Lady Ada Chukwudozie, disclosed this during the MAN South-East Stakeholders’ Industry Conversation held in Awka, Anambra State.

The forum was convened to address concerns surrounding electricity regulation, billing transparency and declining industrial productivity across the region.

Chukwudozie said the few factories still operating were doing so at less than 30 per cent of installed capacity due to soaring electricity tariffs, high energy costs and limited access to credit facilities.

According to her, the harsh operating environment informed the decision to convene the stakeholders’ roundtable, stressing that the manufacturing sector remains critical to economic growth, industrialisation and job creation.

She warned that unless urgent measures are taken to address the challenges confronting manufacturers, industrial activities in the South-East could further deteriorate, with serious implications for employment and regional economic stability.

“The manufacturing sector cannot thrive in an environment of uncertainty,” she said.

She called for reforms in the power sector to be driven by transparency, accountability and measurable performance standards, including agreed electricity supply hours, actual delivery levels and compensation mechanisms where supply consistently falls below expectations.

Chukwudozie also urged regulatory authorities to strengthen oversight of electricity providers and improve power supply to industrial clusters across the South-East.

Stakeholders at the forum expressed concern that manufacturers were increasingly struggling to cope with escalating production costs, worsened by unreliable electricity supply and the rising cost of alternative energy sources.

They noted that without affordable and stable energy, many more companies could either scale down operations or shut down completely.

In his keynote address, former Chairman and Chief Executive Officer of the Nigerian Electricity Regulatory Commission, NERC, Dr. Sam Amadi, urged governments in the South-East to adopt deliberate policies aimed at prioritising electricity supply to industrial clusters.

Amadi also advocated pricing frameworks that would encourage manufacturers to expand production and invest in growth.

The stakeholders’ meeting brought together manufacturers, regulators and other industry players to explore practical solutions to revive industrial output and tackle persistent power challenges affecting businesses in the region.

Nigeria’s oil infrastructure has a habit of telling uncomfortable truths. Not just about barrels and flow rates, but about how a country chooses to value what it cannot afford to lose, and what it risks when it gets that calculation wrong.

Take the Amukpe-Escravos Pipeline, for example. A syndicate of lenders, led by Sterling Bank, is pushing back against efforts to revive a collapsed transaction involving a 40% stake in the asset. Their argument is not complicated. It is rooted in numbers and contractual discipline.

To be clear, a deal that fell apart in 2024 is being reconsidered using a valuation from that same year. However, since then, the asset has proved its worth. Independent assessments now place that stake closer to $600 million. The earlier benchmark sits far below that. The gap is not cosmetic. It is material. And if left unaddressed, it becomes a cost.

The original $243 million offer did not collapse by accident. It was terminated in October 2024 after Conpurex Limited failed to meet payment obligations, breached key terms, and sought to shift risk back to the seller. By the time the Technical Committee closed the process, confidence had already drained out of it. That much is settled.

Ordinarily, that should have been the end. Instead, there are moves to return to a September 2025 approval linked to that same process. The lenders describe this as an administrative carryover. Their response is simple. Start again. Set aside the old approval. Bring in an independent adviser. Return the asset to the market and let current value speak.

What is striking is not just the position itself, but how unusual it sounds in the Nigerian context. In a system where strategic assets have too often travelled through corridors of convenience, an insistence on valuation and process can sound almost rebellious. It should not be so.

Because this is not entirely about one pipeline. It is about whether a terminated deal remains terminated. Whether contracts still mean what they say. Whether performance counts for anything once the paperwork has been filed away. And, crucially, who bears the cost when value is ignored.

The numbers, as always, are blunt. A 2025 independent valuation, referenced in the March 2026 edition of Africa Oil+Gas Report, places the 40% stake at a mid-case of $372 million, a high case of $544 million, and an upside of $641 million. These are not speculative figures. They reflect an asset that has quietly done its job in a difficult environment.

With a capacity of 160,000 barrels per day and uptime consistently above 95%, the Amukpe-Escravos Pipeline has become one of the more reliable evacuation routes in a system where reliability is often in short supply. While other corridors struggle with theft and disruption, this one works.

That fact matters a great deal. Because when an asset proves itself under pressure, its value does not stand still. It moves. To price it as though nothing has changed is not just a technical choice. It is a financial one. And every financial choice has consequences.

It says performance can be ignored. It says time does not count. It says administrative continuity can outrun economic reality. To be fair, the earlier process gave enough warning signs. Lenders questioned the assumptions. Coordination was weak. When Continental Oil and Gas stepped back, Conpurex entered without a clean transition and soon began to reopen settled terms, shifting obligations and introducing new conditions that unsettled the commercial balance. The eventual termination was not dramatic. It was inevitable.

What unsettles stakeholders now is the possibility that a process that ran its course may still shape the outcome. If a concluded transaction can reappear without a clear restart, the line between closure and continuity begins to blur. Once that line blurs, contractual uncertainty follows. And when certainty weakens, serious capital takes notice.

This is where the issue widens beyond the pipeline itself. Back in March, Africa Oil+Gas Report described the Amukpe-Escravos matter as no longer just a transaction story, but a test of how Nigeria governs, values, and safeguards strategic oil infrastructure. That reading feels even more relevant now.

Because what is at stake is not simply who acquires a stake in a pipeline. It is how the country signals to those willing to invest in its most critical assets. It is about whether value is recognised only in theory, or protected in practice. It is about whether losses are acknowledged, or quietly absorbed.

The lenders’ position is often described as resistance. It is better understood as discipline. Reset the process. Revisit the approval. Bring in independent oversight. Return the asset to the market through a transparent and competitive process that reflects present realities. Ensure capable counterparties. Align all stakeholders.

These are not extravagant demands. They are the basics. Nigeria has seen too many assets drift from promise to regret. Too many structures that once worked reduced to cautionary tales. When something works, when something proves resilient in a difficult system, the least that can be done is to treat it with the seriousness it has earned.

Moments like this do not announce themselves as turning points. They arrive quietly, dressed as routine decisions.

But they reveal everything. For an economy seeking disciplined capital and trying to rebuild confidence, the signal matters. Let the process be reset. Let valuation reflect reality. Let the outcome show that when Nigeria recognises value, it also knows how to protect it, and what it stands to lose when it does not.

Until then, the lenders’ position stands as a reminder that in a system where too much has been taken for granted, some lines are too important to be crossed and must be held.

● Sufuyan Ojeifo publishes THE CONCLAVE online newspaper.

-

News3 days ago

News3 days agoXenophobia : Nigerians in South Africa take up arms in self defence

-

News2 days ago

NNAMDI KANU: NMA condemns Prof. Aghaji’s arrest, demands justice

-

News2 days ago

Nigerian students issue 4-day ultimatum to South African businesses to leave the country

-

News3 days ago

Xenophobia: Two more Nigerians killed in South Africa

-

News2 days ago

PFIPC Scandal: New details reveal SGF’s Office cleared Adeyemi for Canada Summit

-

News1 day ago

DSS releases Nnamdi Kanu’s doctor, Aghaji

-

News2 days ago

US planning to use lots of documents against Tinubu — Primate Ayodele

-

News1 day ago

Tiktoker, Peller, arraigned in court for threatening and videoing police officers on duty; granted 500k bail