Business

Marketers oppose Dangote’s move to reduce cooking gas price

President of the Dangote Group, Alhaji Aliko Dangote, has announced plans to reduce the price of Liquefied Petroleum Gas, also known as cooking gas.

He also promised to start direct sales of the product to consumers should the existing distributors fail to allow the price crash in cooking gas.

However, operators in the sector have disagreed with the plan, saying the businessman was planning to monopolise the LPG sector. They kicked against the move on Monday, as the dealers expressed fear of a possible monopoly.

Speaking during a recent tour of his refinery by some local and foreign guests, Dangote stressed that the current price of cooking gas is expensive and not affordable for the common people who depend on firewood for cooking.

He disclosed that the refinery now produces 22,000 tonnes of LPG daily and it is ramping up production for distribution into the Nigerian market, especially as Nigerians move towards the use of gas for cooking.

Speaking to members of the Lagos Business School CGEO Africa, at the refinery in Lekki, Dangote said, “The one that we didn’t write, which you must have seen, is LPG. Currently, we do LPG of about 2,000 tonnes per day. You know Nigeria is gradually moving to the usage of LPG. But I believe it is expensive, but right now we’re trying to bring down the price and make it cheaper.”

Dangote warned that “if the distributors are not trying to bring it down, we’ll go directly and sell to the consumers, so that people will now transit from firewood or kerosene to LPG for cooking.”

Dangote had also announced plans to start the direct distribution of petrol, diesel, and aviation fuel to marketers nationwide in August, with 4,000 CNG-powered buses procured for the exercise.

Currently, the price of cooking gas hovers around N1,000 and N1,300 per kilogramme. Dangote said this would be brought down to ensure affordability.

Operators kick

It appears operators in the LPG market are not pleased with Dangote’s plan to disrupt the sector.

Speaking in an interview with our correspondent, the former Chairman of the LPG and Natural Gas Downstream Group of the Lagos Chamber of Commerce and Industry, Godwin Okoduwa, described the plan as monopolistic.

Okoduwa expressed concern that the billionaire businessman should recognise the fact that some investors grew the market from 70,000 metric tonnes in 2007 to over 1 million metric tonnes in 2022, saying collaboration is the way to go.

“I think it’s monopolistic. I think a market should be protected to encourage growth. The LPG industry in Nigeria grew from 70,000 metric tonnes in 2007 to over 1.3 million tonnes in 2022. That was done by collaboration — collaboration with the Federal Government, the NLNG, and offtakers. Everything was done in collaboration. It grew from 70,000 to 250 to 800, and now over a million,” Okoduwa said.

He stressed that growth cannot be achieved through a monopoly but through collaboration. “Today, we are just under 5kg or 6kg per capita consumption in terms of LPG. Other countries are doing much more. South Africa is doing double digits, Morocco and Tunisia are doing double digits. We can do much more.

“So, we should, as an industry and as a country, focus on how to grow the LPG industry and not allow someone (to frustrate the players). Yes, he has invested; yes, it’s a capital economy, but he should not be allowed to frustrate the players.

“There are people who have spent money, spent resources, even business and development, and someone just comes in to reap from the work that has been done. I’m sure he wouldn’t have built if there had not been an existing market. The work has been done, he should respect the market and let us grow. It shouldn’t be a zero-sum strategy. It should be collaborative,” he said.

In his recommendation, the gas expert said that though Dangote has the upper hand, he should embrace collaboration.

“My advice to him is that the pie can be bigger. The Nigerian market is about 1.3 million tonnes. The Nigerian LPG market can be 5 million tonnes. He should work towards collaboration rather than competition, because at the end of the day, everybody benefits,” he added.

Told that Dangote’s major concern is to bring the price of cooking gas to a rate where everybody can afford it and stop cooking with firewood, Okoduwa retorted, “I have news for him. He should go to the Northeast, where you have the least consumption of LPG. He should go to the Northeast and start developing the LPG infrastructure there. I think we will tell him thank you for that.”

Similarly, the Executive Secretary/Chief Executive Officer, Nigerian Association of Liquefied Petroleum Gas Marketers, Bassey Essien, doubted the possibility of Dangote selling gas directly to consumers or to crash the price.

“I am saying that it’s unrealistic. What is the position with PMS? Has the refinery been able to sell petrol directly to you and me into our cars at a very cheap rate?” Essien asked.

(PUNCH)

The Yenagoa Division of the Federal High Court on Friday dismissed a suit challenging the divestment of Shell from onshore assets.

The suit filed by King Bubaraiye Dakolo, traditional ruler of Ekpetiama in Yenagoa Local Government Area of Bayelsa also sought redress and remediation of cumulative pollution of Dakolo’s domain for 40 years.

Dakolo alleged that the divestment by Shell did not follow the stipulated guidelines in the Petroleum Industry Act (PIA) 2021.

However, presiding judge, Justice Ayo Emmanuel in a ruling dismissed the case for being filed out of time adding that under the statute, any objections to divestment on guy to be filed within three months.

Emmanuel also held that the traditional ruler lacked the ‘locus standi’ to institute the case as he had no role in the divestment.

The judge further stated that the plaintiff failed to explore and exhaust the conflict resolution mechanism mechanisms by the Nigerian Upstream Petroleum Regulatory Commission,

The judge noted that the failure according to the Petroleum Industry Act (PIA)asked the suit invalid.

“Plaintiff’s failure to satisfy the mandatory statutory conditions precedent under the Petroleum Industry Act (PIA) strips this Court of jurisdiction.

“The Plaintiff further contended that the injuries complained of constitute a “continuing injury, thereby creating a continuous cause of action that escapes the limitation periods.

“However, looking closely at the pleadings, the Plaintiff joins historical grievances stretching back decades with specific events that allegedly took place around 2024. A continuous injury means a recurrence of the legally wrongful act itself, not the continuous persistence of the injurious effects of a singular past act.

“From the facts presented, the alleged causes of action against the public officers (the 4th, 5th, and 6th Defendants) arose well outside the mandated 3-month period prescribed by POPA.

“Furthermore, the claims touching on tortious liability are caught by the 5-year limitation threshold under Section 16 of the Limitation Law of Bayelsa State,” Emmanuel ruled.

Reacting, Counsel to the Minister of Petroleum Resources, Lawrence Edet who spoke for the defendants thanked the court for dispensing justice to their favour.

Counsel to Dakolo said that they will pursue the case beyond the trial court and will be heading to the court of appeal.

Environmental justice group, Social Action in its reaction to the judgement expressed regret that the court had to ignore the quest for environmental justice and technicalities.

Dr Prince Edegbuo

Resource Justice Manager at Social Action said: “It is very very unfortunate that a matter as important as this that is gaining international traction in home countries where these international companies come from and the activities being condemned but our legal system finds it convenient to discard a case that has caused so much hardship and suffering on the people.

“The pollution had devastated the environment and denied people of their livelihoods and even affected the reproductive health of the people, it is heartbreaking that the Federal High Court struck out this case.

“We will meet at the Appeal Court, we will not relent, we shall continue to support the Ekpetiama people in this litigation, this is just the court of first instance,” he said.

Ekpetiama community is in the neighbourhood and part of host communities to the Gbarain-Ubie gas plant and Gbarain oilfields.

Listed as defendants in the suit No. FHC/YNG/CS/81/2025, are Shell Petroleum Development Company of Nigeria, Shell Petroleum N.V, Shell UK PLC.

Others are Attorney General of the Federation, The Nigerian Upstream Petroleum Regulatory Commission, Minister of Petroleum Resources and Renaissance Energy Africa Ltd.

It will be recalled that Renaissance Energy Africa, a consortium of indigenous oil firms in March 2025 acquired the onshore and shallow waters oil and gas assets hitherto operated by SPDC, following the divestments by Shell UK PLC, the parent company to SPDC.

•Says illegal goods on Dangote trucks to be confiscated

Dangote Industries Limited has intensified efforts to combat illegal haulage activities involving its trucks by unveiling a public whistleblowing initiative that offers a cash reward to individuals who provide credible information leading to the arrest of offenders or the interception of unauthorized goods and transportation of persons.

The company said the initiative, which will reward whistleblowers with N500,000.00 cash award, forms part of its broader commitment to protect the integrity of its logistics operations and eliminate the activities of unscrupulous individuals who illegally use Dangote-branded trucks to transport unauthorized goods.

In a statement issued in Lagos, the management urged members of the public to support the campaign by reporting any suspected cases of illegal haulage involving Dangote trucks, stressing that only specifically approved products are permitted to be transported by vehicles belonging to its various subsidiaries.

Dangote trucks

According to the company, Dangote Cement trucks are authorized to carry only cement, limestone, high-grade gypsum, coal and clinker, while Dangote Sugar Refinery trucks are restricted to the transportation of sugar products. Trucks belonging to NASCON Allied Industries are expected to carry Dangote Salt and DanQ Seasoning products, while Dangote Packaging vehicles are designated for bags and packaging materials.

Similarly, trucks operated by Dangote Petroleum Refinery and Petrochemicals are permitted to transport polypropylene products, while Dangote Fertiliser Limited vehicles are authorized for the haulage of urea fertilizer.

The company warned that any Dangote truck found transporting unauthorized goods would be treated as being involved in illegal haulage activities, adding that both the drivers and owners of such goods risk arrest, confiscation of the cargo and prosecution under applicable laws.

“Anyone with verifiable information that leads to the arrest of persons involved in illegal haulage activities or the recovery of unauthorized goods transported on Dangote trucks will receive a cash reward of Five Hundred Thousand Naira,” the company stated.

To aid investigations and enforcement efforts, the management of Dangote Group advised whistleblowers to provide detailed information when making reports. These include the truck type, registration plate number, cab number, location of the vehicle, description of the goods being transported, colour of the truck and photographs of the vehicle and cargo where possible.

The company has therefore established dedicated hotlines across its operations to receive reports relating to illegal haulage activities. Members of the public can report incidents involving trucks operating from the Obajana, Okpella and Gboko plants through certain dedicated telephone lines.

The Company stated that law enforcement agencies, including the Police, have been authorized to arrest any driver found using company trucks for unauthorized commercial haulage.

It reiterated its zero-tolerance stance against logistics-related fraud and called on the public to join hands with it in safeguarding legitimate business activities by exposing illegal operators.

Dangote Group emphasized that the initiative is designed not only to protect company assets and operations but also to strengthen transparency, accountability and compliance across its nationwide logistics network.

“Public cooperation remains critical in our efforts to eradicate illegal haulage activities. We encourage anyone with credible information to come forward and help us maintain the integrity of our transportation system,” the statement added.

The company reaffirmed that all reports would support ongoing efforts to protect the Dangote brand, promote lawful business practices and ensure that offenders are brought to justice.i

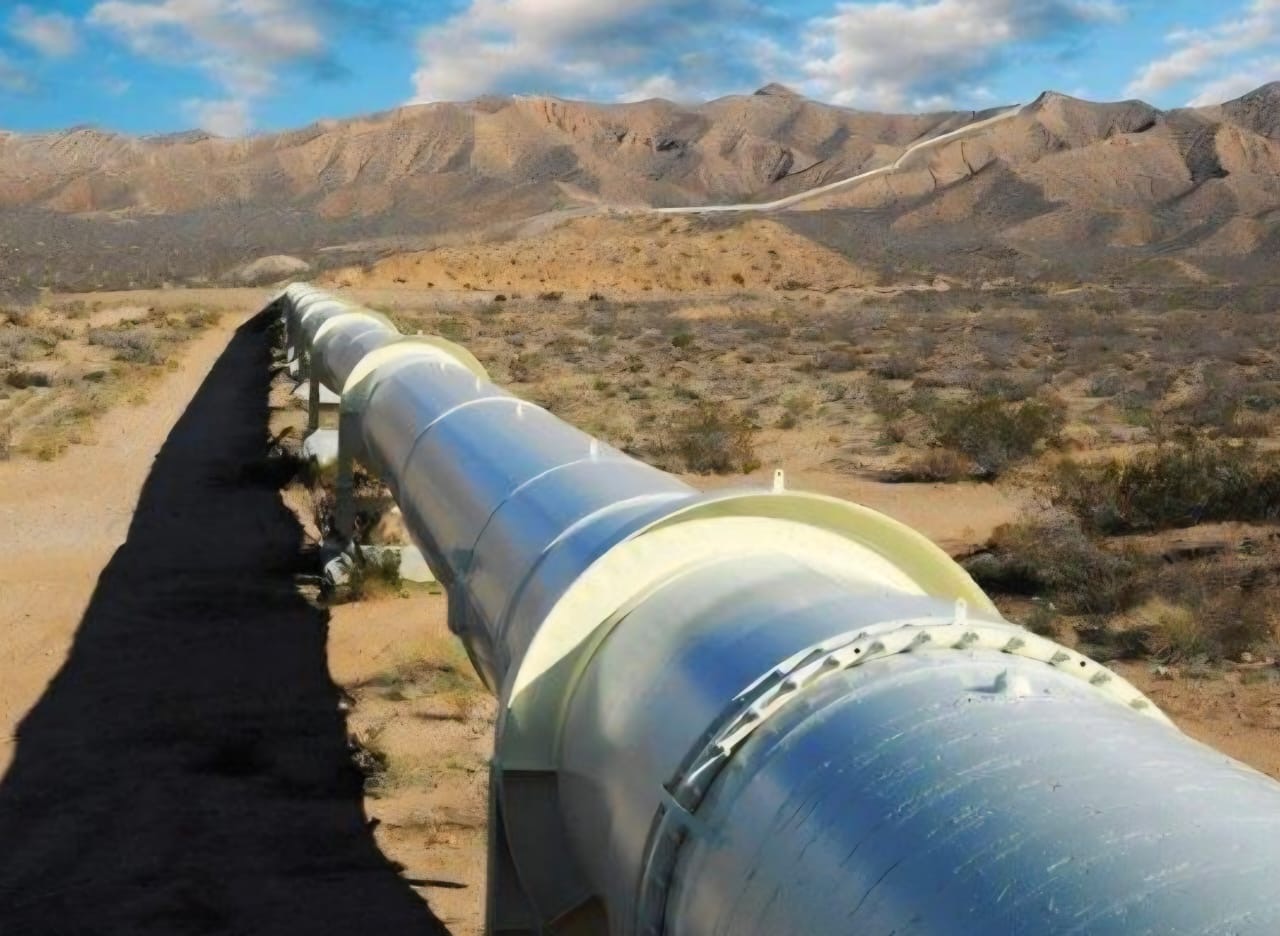

Fresh controversy has erupted over efforts to revive the sale of a 40 per cent stake in the Amukpe–Escravos Pipeline, with a governance expert warning that any attempt to resurrect a previously terminated transaction could damage investor confidence and raise fresh questions about transparency in Nigeria’s oil and gas sector.

Speaking on Channels Television on Thursday, June 11, 2026, Managing Director of Policy Management Consult Services, Jide Olatuyi, said concerns surrounding the transaction extend beyond commercial interests and strike at the heart of governance, transparency, and the credibility of Nigeria’s investment environment.

“The contract was terminated,” Olatuyi said. “What stakeholders are saying is that there is a need for a new competitive bidding process rather than attempting to revive a failed transaction.”

The controversy has intensified amid scrutiny of the asset’s valuation. The earlier transaction involving the 40 per cent stake was priced at approximately $243 million before collapsing over unmet contractual obligations. Independent assessments conducted in 2025 reportedly valued the same stake at between $544 million and $641 million.

The significant disparity between the earlier transaction price and the more recent valuations has fuelled calls for a fresh competitive bidding exercise to ensure that the asset reflects prevailing market conditions and delivers maximum value.

Rejecting suggestions that opposition to the proposed transaction is driven by sentiment or commercial rivalry, Olatuyi insisted that the debate centres on governance standards within the petroleum industry.

“I don’t think it is about sentiment at all,” he said. “It is about governance in the oil and gas sector.”

According to him, Nigeria’s challenge is no longer limited to attracting investors but also ensuring that investors have confidence in the integrity of the country’s commercial and regulatory processes.

“If you are not committed to transparency, it becomes a problem for investors,” he said. “If you cannot build trust and confidence in the sector, capital will go elsewhere.”

Olatuyi said several stakeholders, including project lenders such as Sterling Bank and AMCON, have advocated a transparent process that reflects current market realities and updated asset valuations.

The Amukpe–Escravos Pipeline, which has a transportation capacity of about 160,000 barrels per day and has maintained uptime above 95 per cent, remains one of Nigeria’s most strategic crude evacuation assets. The pipeline plays a critical role in transporting crude from inland production fields to export terminals in the Niger Delta.

Olatuyi urged authorities to ensure that any future transaction involving the asset is conducted through an open, transparent, and competitive process capable of inspiring investor confidence and safeguarding public value.

The debate comes at a time when the Federal Government is seeking to attract substantial investment into the energy sector and expand critical oil and gas infrastructure.

The eventual outcome of the Amukpe–Escravos Pipeline transaction could serve as a major test of Nigeria’s commitment to transparency, valuation discipline, and investor protection. As global competition for energy capital intensifies, governance standards may prove just as important as resource endowment in determining where investment flows.

Officials of the Nigerian Upstream Petroleum Regulatory Commission and members of the technical committee that supervised the original transaction did not respond to requests for comment as of press time.

-

News1 day ago

News1 day agoGunmen kill four herders from same family, raze cattle camp, slaughter cows in Anambra

-

News2 days ago

Plateau gov apologises to Igbo over civil war

-

News1 day ago

PFIPC Probe: Why Tinubu’s Chief of Staff, Head of Service, Accountant-General should step aside — Opara

-

News1 day ago

Deputy Speaker Kalu breaks silence on N780m Budget controversy, says Fund not meant for Churches alone

-

News3 days ago

ICPC grills Gbajabiamila over PFIPC scandal

-

News2 days ago

Enugu Air Showcases Investment Vision at Farnborough International Airshow

-

News1 day ago

Gov Mbah flags off distribution of farm inputs to 63,000 Enugu farmers

-

News3 days ago

Enugu Gov’t to distribute Agric Inputs to 63,000 Farmers